<br />

<b>Deprecated</b>: strip_tags(): Passing null to parameter #1 ($string) of type string is deprecated in <b>/home/digitalr/robotsthink.com/wp-content/themes/Newspaper/loop-single.php</b> on line <b>64</b><br />")

[ad_1]

Bloomberg/Bloomberg through Getty Pictures

Palantir Applied sciences’ (NYSE:PLTR) This autumn earnings confirmed an acceleration in its US business enterprise because it closed out its first GAAP worthwhile 12 months. Shares are reflecting the optimism surrounding Palantir’s business section and backside line enlargement, with shares up greater than 47% YTD and almost 280% because the begin of 2023.

We famous in our inventory e-newsletter in December that Palantir was “exhibiting a number of indicators of acceleration heading into 2024 with an improved elementary backdrop pushed by rising AI demand. Palantir’s Synthetic Intelligence Platform (AIP) is driving a major acceleration in its US business enterprise, whereas underlying metrics and the underside line are quickly enhancing.”

Income acceleration stemming from the business enterprise is the most important story for Palantir by means of 2024 and into 2025, with income development poised to speed up from 17% final 12 months to twenty% this 12 months and almost 21% in 2025.

Robust Acceleration in US Industrial Is Driving Development

In a deep dive on the time of Palantir’s direct itemizing, our agency stated in 2020 that the “business sector is the expansion story.” Palantir’s public providing was seen as a strategy to facilitate attracting and buying business shoppers earlier than AI introduced a wave of competitors. The fruits of Palantir’s labor are starting to repay, with a newfound speedy acceleration in its US business enterprise after AIP’s launch in Q2 was met with “unprecedented” demand. At its core, Palantir’s AIP is a complete AI resolution that lets clients lever Palantir’s AI and machine studying instruments and harness the facility of the newest massive language fashions (LLMs) inside Foundry and Gotham. Clients can deploy LLMs on their very own personal networks utilizing their very own personal information, maximizing information safety and enhancing effectivity by serving to cut back information switch and storage prices.

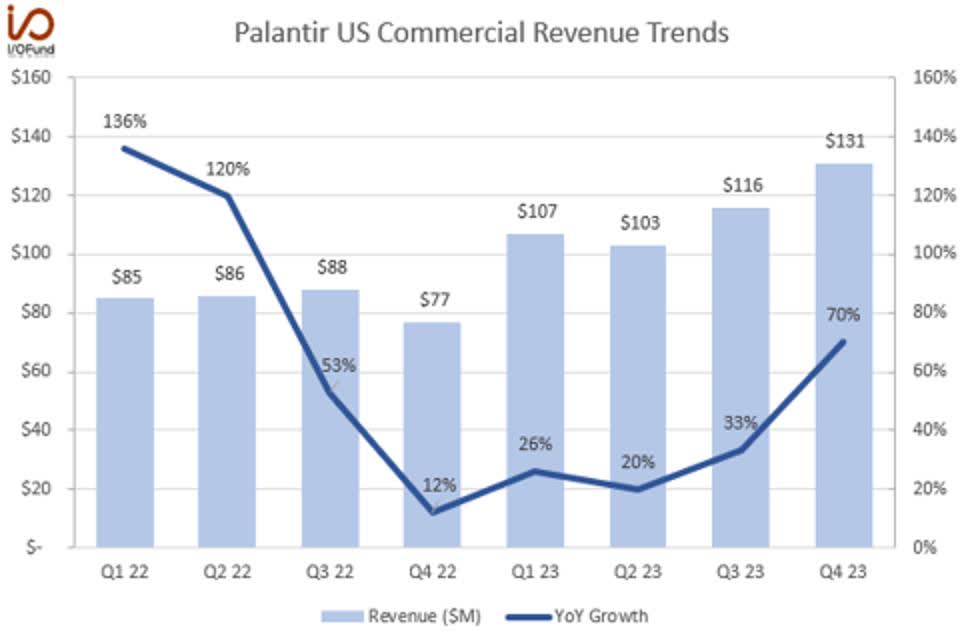

Though its US business section accounts for lower than 25% of quarterly income — it simply surpassed a $500 million annual run fee in This autumn — it’s now changing into the dominant issue behind the sturdy enterprise momentum Palantir has seen over the previous few quarters.

US business income rose 70% YoY to $131 million, a 37 share level acceleration from Q3 and a 58 share level acceleration from the 12 months in the past quarter. For the complete 12 months, US business income rose at greater than double Palantir’s development fee, rising 36% YoY to $457 million.

The graph beneath illustrates simply how sturdy the latest quarter was:

PALANTIR

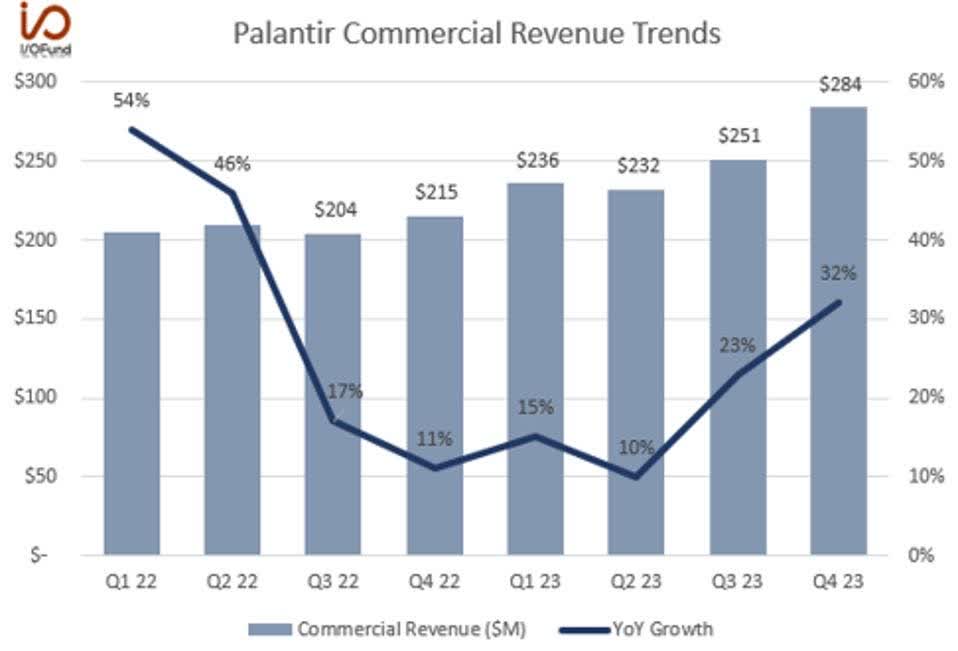

This acceleration within the US over the previous two quarters is driving world business income greater. Palantir’s world business income accelerated by 22 share factors, from 10% development in Q2 to 32% in This autumn. The section topped a $1.1 billion annual run fee final quarter, up from a $920 million run fee two quarters in the past.

PALANTIR

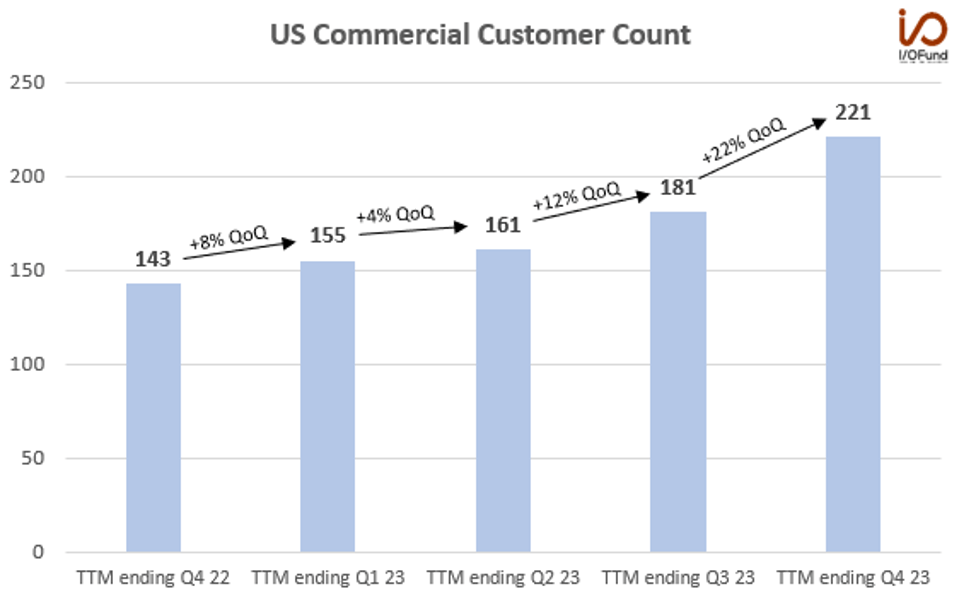

Whereas the income acceleration was the principle headline for the US business enterprise, a better look reveals that the section additionally drove greater than 90% of Palantir’s buyer additions with very sturdy underlying metrics.

Palantir reported 55% YoY and 22% QoQ development in US business buyer rely to 221 within the quarter, as buyer development continues to speed up. Over the previous two quarters, Palantir has added 60 internet new US business clients with 40 clients added in This autumn alone. That is greater than 3X greater than the earlier interval of simply 18 internet new US business clients from This autumn 2022 to Q2 2023.

PALANTIR

World business clients elevated 44% YoY and 14% QoQ to 375 clients – representing 45 internet new buyer additions within the quarter. This implies the US business section drove greater than 90% of Palantir’s internet new buyer additions in This autumn. That compares to beneath 63% of internet new buyer additions in Q3 and simply 20% in Q2.

This development was “meaningfully pushed by AIP” with Palantir saying that “demand is off the charts” for its new product. AIP is “propelling development each by means of new buyer acquisitions and expansions with present clients,” with proof of AIP bootcamps “serving to to considerably compress gross sales cycles and speed up the speed of recent buyer acquisition.”

Palantir had set a objective in October to hit 500 AIP bootcamps to drive prime of funnel development, and it has already surpassed that concentrate on, finishing 560 bootcamps in simply 4 months.

CRO Ryan Taylor commented on how this interprets by means of to development within the US business section, with

“70% year-over-year development in income in This autumn, 55% development in buyer rely year-over-year, and a 107% development in TCV closed on an adjusted foundation […] Both it is — first, its bootcamps which might be shortly changing to paying clients or its enlargement of present clients or its clients the place perhaps we have been engaged for some time and introduction of AIP, that complete course of has been accelerated. We’re seeing that throughout the board, and but on the similar time, we barely touched that addressable market.”

Partaking clients through bootcamps to then translating that engagement into new buyer offers or expanded offers units the muse for sustained income development at the next fee, extra so if it may possibly drive its internet retention fee greater.

A Be aware on Internet Retention Fee

Palantir reported a company-wide NRR of 108% in This autumn, however famous that it “doesn’t but totally seize the acceleration in our US business enterprise” since clients acquired over the past twelve months are usually not mirrored within the calculation. A majority of the online new buyer additions have come within the final two quarters, suggesting US business NRR can be greater than 108% come the tip of FY24 when this buyer cohort is mirrored. For context, Palantir reported an NRR of 150% on the finish of FY21 in US business, however that seemingly fell considerably when development slowed to a crawl on the finish of FY22.

If AIP can proceed to drive a excessive degree of buyer acquisition and enlargement by means of FY24, this might help drive and keep the income acceleration we’re seeing within the section by means of FY25 and into FY26.

Valuation Stays a Danger Regardless of Robust Enchancment in Fundamentals

Basically, Palantir has seen main enhancements all through FY23, because it turned the corporate’s first GAAP worthwhile 12 months.

Gross margin has expanded constantly all year long, rising 300 bp YoY from 79% to 82% in This autumn. GAAP working margin shifted constructive and expanded in every quarter in 2023, rising from (4%) in This autumn 2022 to 11% final quarter.

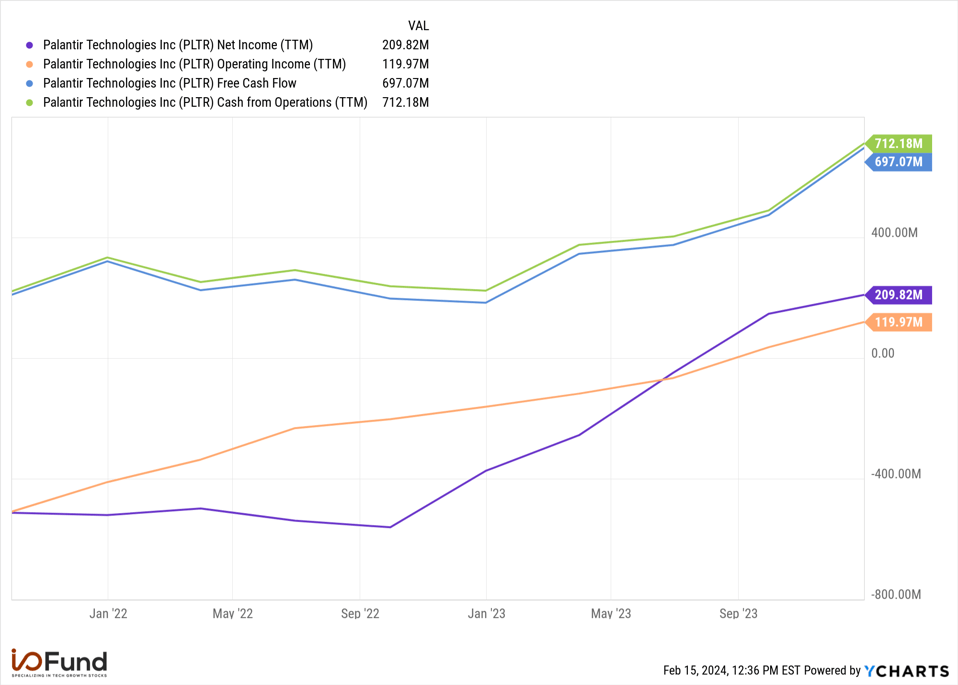

Internet revenue development has been notably sturdy, with Palantir producing almost $210 million in internet revenue throughout the 12 months, in comparison with almost ($374 million) in 2022. Money circulation technology has improved considerably, with working and free money circulation each greater than doubling QoQ in This autumn to over $300 million. Palantir ended the 12 months with a 32% OCF margin and a 33% adjusted FCF margin.

YCHARTS

Whereas the basics are actually supporting a rise in Palantir’s share value, the AI hype could also be overshooting the near-term potential for returns at this degree. What’s putting is that traders are paying costs final seen when the market set a serious prime in November 2021, in the meantime the 2021 development story is decoupled from administration’s long-term 30% income development goal.

In early 2021, Palantir’s administration anticipated to achieve $4 billion in income by 2025 as they anticipated greater than 30% annual income development annually for the following 5 years, or by means of 2026. Palantir exceeded this goal with 34% development in 2021, however a macro-inflicted deceleration in late 2022 and early 2023 has virtually nullified its means to achieve that $4 billion goal after posting 24% development in 2022 and simply 17% in 2023. Present analyst estimates level to almost 21% development to $3.22 billion in income in 2025, which means Palantir is one 12 months off observe – it’s projected to achieve the $4 billion milestone in 2026, one 12 months later than anticipated.

To succeed in $4 billion by the tip of 2025, Palantir would want to file 35% development this 12 months and subsequent, about 15 share factors above estimates for each years. Whereas AIP is aiding sturdy acceleration within the US business section, it’s unlikely to drive revenues to that concentrate on. Because of this, shares could also be pricing in perfection for AIP and AI-related inventory efficiency.

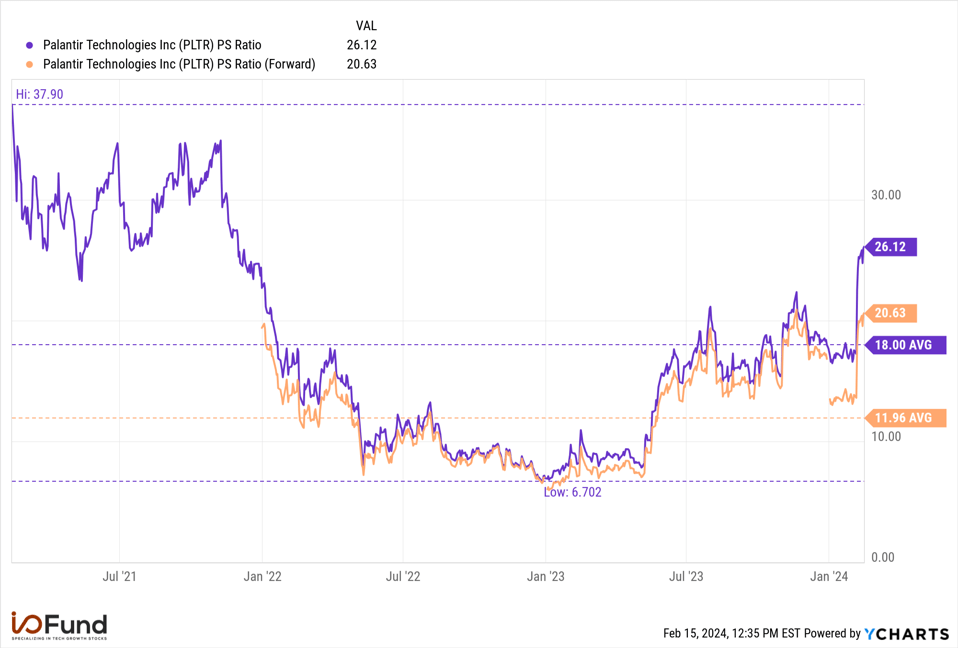

YCHARTS

Previous to This autumn’s earnings, Palantir was buying and selling close to its common P/S ratio of 18x, however the sturdy rally has now taken shares to over 26x P/S and 20x ahead P/S – that is the best degree since late 2021 but development has slowed. On a money circulation foundation, shares are buying and selling at round 60x 2024’s projected $800 million to $1 billion in adjusted FCF.

Palantir’s shares are not low-cost. It’s the third most costly enterprise software program inventory on a ahead P/S foundation, behind Cloudflare and Snowflake, regardless of having the slowest ahead income development fee by greater than 700 foundation factors, at 20% in comparison with 27% to 30% for the opposite two. This valuation might open up the door for draw back all year long because it leaves no room for error, contemplating its decrease income development fee in comparison with friends; as well as, any dampening to development inventory sentiment from higher-for-longer charges with minimize expectations being pushed again additional within the 12 months additionally presents a possible headwind for shares.

Conclusion

Enterprises are displaying elevated curiosity in Palantir’s Synthetic Intelligence Platform, which is translating to new buyer additions. AIP’s early success within the US business section drove Palantir’s new buyer additions in This autumn. US business income is accelerating considerably, reaching 70% YoY development in This autumn from 33% within the prior quarter.

Administration’s commentary about how Palantir is participating and changing clients through bootcamps units a basis for a sustained acceleration due to a speedy buyer acquisition cycle. Nonetheless, the scale of the US business enterprise at lower than 25% of quarterly revenues signifies that the AI-related acceleration is probably not sufficient to maintain the inventory’s present valuation.

Tech Insider Community Fairness Analyst Damien Robbins contributed to this evaluation.

Really useful Studying:

[ad_2]

Supply hyperlink